Cracking the 0DTE Code, Part 4: RVOL

3 min read · Just now · by Adam · Read Part 1 · Read Part 2 · Read Part 3

I now use time-adjusted RVOL primarily as a real-time participation filter, especially during the pre-market session and the first five to ten minutes after the opening bell. Weak relative volume can warn that an otherwise valid bullish or bearish day-type expectation lacks enough participation to produce immediate continuation. Expanding relative volume can then confirm either continuation or reversal, depending on how the accompanying candle reacts to a key level such as PMH, PML, YDH, or YDL.

The updated framework is therefore not simply “divergence plus RVOL.” The day type provides the expectation, the key level provides the location, price action provides the direction, and RVOL shows whether meaningful participation has arrived.

The TradingView indicator I currently use is Relative Volume (rVol), Better Volume & Average Volume Comparison .

In practical terms, low-participation bars mean patience. A relative-volume expansion means the current price event deserves attention, but RVOL itself is not inherently bullish or bearish.In Part 3, we introduced options premium divergences with the underlying (SPY), including extrinsic divergences, and built a ToS indicator to apply the study to both call and put charts across SPY strikes. Those divergences help spot when volatility expectations begin shifting ahead of SPY’s next move.

Now we’re adding the missing piece of confirmation: Relative Volume (RVOL).

RVOL measures how active today's trading is compared to its usual pace for that same time of day. An RVOL of 1.0 on the 1-minute chart marks average participation. Above 1.0 signals show heightened participation, while below 1.0 indicates participation is running below its normal pace for that time of day. On the 5-minute chart, a stronger threshold of 2.0 better filters out noise and highlights genuine bursts of activity. In 0DTE trading, RVOL confirms when dealer hedging or large directional flow actually hits the tape.

🕒 Why some divergences “lag”

If you’ve used the indicator already, you’ve noticed BULL/BEAR EX can sometimes fire early, especially 12:30–15:00 ET. After the trigger, SPY may drift for 5–15 minutes, putting option contracts in drawdown before the expected move accelerates. That delay isn’t rando. It’s the dealer gamma/theta cycle through the day.

Morning (09:30–10:15): IV decompressing, hedges lagging

- Dealers are still building and balancing 0DTE inventory from the open. IV often stays elevated and begins compressing faster than price recovers.

- EX signals can appear early as IV normalizes, but dealer hedge adjustments lag. Signals are rare and can drift before confirming.

Mid‑day (10:30–14:30): Peak γ pin

- Books heavy with short‑gamma exposure.

- Hedges wait for confirmation → 5–15 min lag from EX signal to price response.

Afternoon (15:00+): γ collapse → Δ‑dominant

- Gamma evaporates; hedging becomes linear.

- Responses are immediate; options trade like stock (amplified).

MM Gamma Exposure

│

│ ████████████ ← Mid‑day: Peak pin zone

│ ███████████

│ █████████

│ ██████

│ ████

│ ███

│ ██

│█

│

└───────────────────────────────────────── Time (ET)

09:30 11:00 13:00 15:00 16:00🧠 Dealer logic (bullish case)

- Signal: Extrinsic drops (IV compression) while SPY forms a higher low.

- Posture: Dealers short puts → short SPY to hedge. They stop selling but don’t buy yet → slight drift lower.

- Decay: IV and theta bleed puts; dealers’ delta shrinks.

- Unwind: Over‑hedged short SPY → they buy to rebalance → rally.

Mirror this for the bearish case with short calls and long‑SPY hedges unwinding via selling.

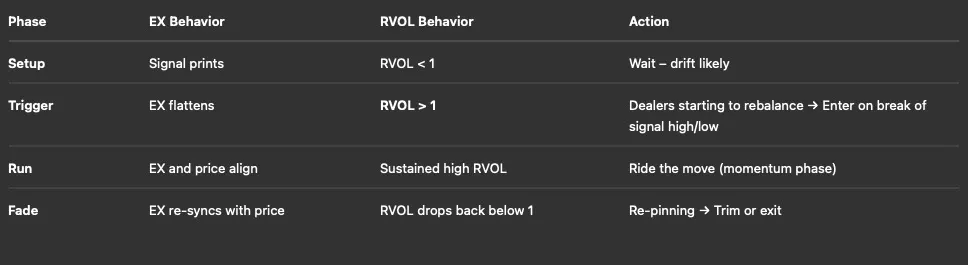

💡How RVOL solves the timing problem

The divergence shows when volatility compression starts.

RVOL shows when hedging flow hits the tape.

Closing thoughts

The extrinsic divergence reveals the setup. RVOL reveals the timing. When both align, you’re not guessing, you’re trading in sync with the dealer hedging cycle itself.

Is this the “price and time” that ICT was talking about all along?